Generic railway strategies TOCs

train operator strategies

a research-oriented knowledge base for train operating companies (TOCs)

a research-oriented knowledge base for train operating companies (TOCs)

As a result of EU’s railways reforms Europe’s railway conglomerates have been financially alleviated by national authorities during voluntary restructuring process in the middle of the 1990s. Billions of debts were transferred from newly formed legal railway entities to national bodies (National Economic Research Associates, 2004, p. 42). In 2011 the financial performance of the conglomerates varied heavily.

Because of their historic roots, incumbent TOCs possess numerous intangible strategic resources. First, their enormous hub and spoke network with coverage of all important national lines (comparable to full-cost airline’s network) allows them to attract customers for smooth train journeys (KSF 5). Second, especially in the areas of route evaluation (KSF 1) and rolling stock procurement (KSF 2) they tend to have advantages over new challengers. Third, their path dependency offers them close connections to important players in the industry. If long-distance TOCs are still part of a vertically integrated conglomerate, they can access know-how from nearly all value system activities as well as influence decisions of important value system players. Moreover, flexible reactions in cases of disruptions (e.g. delays in schedule) and problem solving capabilities are on the incumbent side.

The major weakness of incumbent TOCs lies in the field of human resources heavily affected by companies’ legacies. The reason comes from the companies’ historic paths with heavy restructuring initiatives during railway liberalization since the middle of the 1990s. Numerous jobs were cut and in all former railway conglomerates and workforce numbers were reduced drastically (Friebel et al., 2008, p. 80). Today incumbents suffer from those efforts because numerous employees out of those times are still part of incumbents’ regular workforce. Therefore, they do not always support ambitious management goals in terms of further restructuring to achieve competitive cost structures or developing services and shifting to leaner operations (Roland Berger Strategy Consultants, 2011, p. 14).

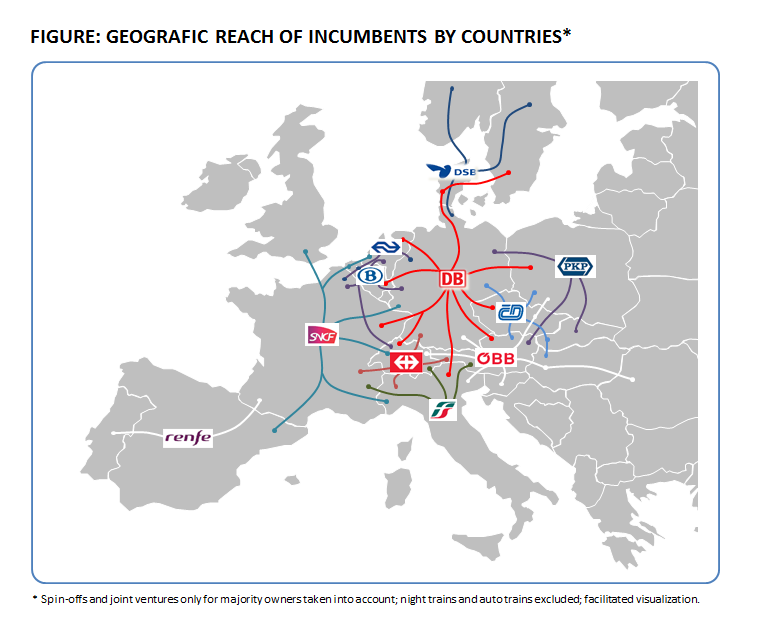

In the past nationally-framed market structures complicated cross-border traffic for long-distance TOCs. As a result strategic activities of incumbents focused on close cooperation among each other to allow international passenger traffic across borders. Thereby, a crucial vehicle was the establishment of joint ventures and new companies.

Every strategic vehicle bears potential advantages. In joint ventures under established companies’ brands every participating incumbent is able to generate knowledge related to operations in the market of the other incumbent. Independently branded venture companies seem to facilitate operations with more than one foreign country involved because of high operational distance to specialize on international issues without path dependency. Independently branded spin-off companies of a single incumbent often possess an exclusive focus such as low-cost or outstanding on-board activities (iDTGV by SNCF). New knowledge and insights can be generated that allow the incumbent to better position itself in a truly competitive market in the future. Moreover, spin-off companies offer the potential to experiment with issues related to key success factor. For example the implementation of a new pricing as well as yield management system could be tested in a spin-off and later on transferred to the incumbent company.

Besides partnering and spin-offs, a major strategic vehicle to increase a long-distance TOCs strategic position is organic expansion into new markets. To be able to grow organically, necessary train capacities must be available. Because of different specifics of the international rail network configuration every train is required to be separately homologated for every country to operate in and requires consequently special technical setups (Müller, 2011, p. 2). As a consequence, trains used in a domestic market cannot simply be utilized for international traffic.

The geographical focus allows to judge on strategic compensation possibilities in case of being attacked in one market. The geographical analysis reveals that established cross-border traffic is always connected to the operating incumbent’s national network. International routes to foreign countries can be classified as spokes to increase the incumbent’s network range. Regular maintenance in this model seems to be executed in the domestic country of the incumbent. Only a few facilities in foreign countries are possessed by network extending incumbents mainly for small maintenance and staff breaks.

A related event in the option field of acquisitions was the announcement of Veolia Environnement in November 2011 to sell its transport division named Veolia Transdev. Because the transport division offers lowest economies of scale potentials compared to other business units of Veolia, the French company decided to streamline its product portfolio, sell its 50 percent share in Veolia Trandev and focus on water, waste and energy services (Railway Gazette, 2011k, p. 1). Veolia Transdev operates urban services in 28 countries on five continents and offers comparable potentials as Arriva (Veolia Transdev, 2012, p. 1).